The share of employers offering student loan repayment benefits is climbing as companies hope to gain a competitive advantage in recruiting younger workers in a still-tight labor market.

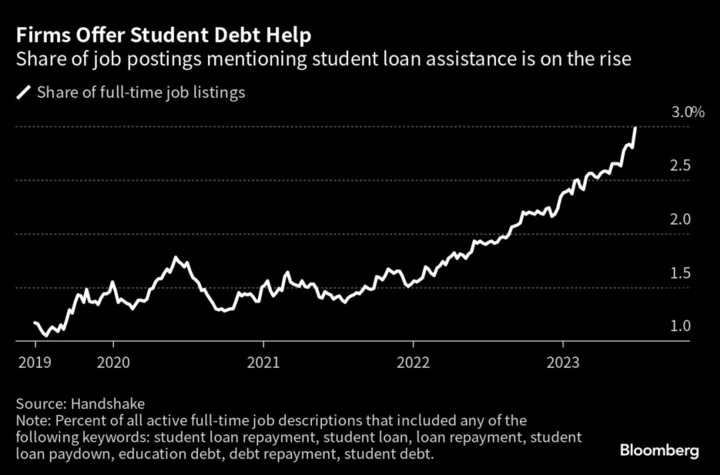

The share of full-time job listings mentioning student debt repayment programs has more than doubled since 2019, according to an analysis by job site Handshake. The benefit, though, is still relatively rare: It shows up in only 3% of job posts.

Christine Cruzvergara, Handshake's chief education strategy officer, expects to see more employers start offering the benefit in the next year or two as student loan payments worth about $1.5 trillion resume for some 28 million US borrowers. The monthly payments are starting up following a three-year pandemic hiatus.

The debate over student debt relief dominated headlines earlier this year when President Joe Biden's plan to slash balances for more than 40 million Americans was rejected by the US Supreme Court.

Last week the administration launched a fresh effort, opening applications for a new income-driven repayment plan meant to shore up low-income borrowers.

Read more: Student Debt Relief Drives More Grads to Teach for America

Some company-sponsored student loan repayment assistance has been around for years, but a few have since stepped up their commitment. Financial services firm Fidelity Investments, which began providing assistance in 2016, raised the program maximum in the fall of 2021. Eligible staff working at least 30 hours a week can now access up to $15,000 over seven years’ worth of monthly payments. The perk helps with higher retention of younger career employees, according to Megan Bourque, head of benefits at the firm.

With a cohort of workers increasingly burdened by student debt, help paying it down is likely to have wide appeal, Cruzvergara said. “Student loans impact their ability to settle down, their ability to buy a home and their ability to, quite frankly, kickstart their entire life,” she said. “It’s such a large swath of our graduating class now that it's undeniably an issue for an entire generation.”

Read more: Chaos Looms as $1.5 Trillion Student-Loan Pause Abruptly Ends

Over half of the class of 2024 expect to graduate with student debt, according to a survey by Handshake of over 1,100 students pursuing bachelor’s degrees at 440 institutions. Of those, almost 70% say their debt will influence which jobs they apply for.

That’s true for Olivia Bianic, an art major at Saint Mary’s College of California. Bianic expects to owe around $20,000 upon graduation, just under the national average. Making a living as freelance artist by creating work she cares about on commission is her ultimate dream job.

While Bianic always knew a career as an artist would never be easy or a sure thing, her level of student debt is making that path even more arduous. For now, that means finding a stable, full-time job with a steady paycheck that allows her to make art on the side. One big selling point, she says: an offer for a job that provides benefits to help her pay down her student debt.

Read more: Borrowers With $39 Billion in Student Loans Finally See Relief

The industries that account for the most listings that advertise student loan help on Handshake include health care and services, nonprofits, and government, law and politics.

It may be an especially smart tactic for companies in less-flashy industries, like insurance or accounting, to adopt. “Because if you're not going to be able to necessarily appeal to the fun, energetic, sexy sort of vibe of your industry, you might as well appeal to the practicalness of what it is,” Cruzvergara said. “I think we're going to start to see it come into play in more industries.”